FHA house hacking is a strategy gaining traction that cleverly combines homeownership with property investment using an FHA loan. For the uninitiated, imagine buying a multifamily home, living in one unit, and having tenants in the other units pay your mortgage. Sounds ideal, doesn’t it? This is precisely what FHA house hacking offers.

The Federal Housing Administration (FHA) loan provides an unparalleled opportunity. With minimal down payments and flexible credit requirements, this method can be ideal for those eager to invest in property without being entirely submerged.

If the idea of generating passive income while securing your own residence appeals to you, then diving deep into the details of FHA house hacking might be the stepping stone you’ve been searching for. Let’s get to it!

What is House Hacking?

The term “house hacking” might evoke images of someone cleverly bypassing the traditional pathways of real estate, and, in essence, that’s precisely what it represents. House hacking is a strategy that real estate investors use to lessen or even entirely offset their living expenses. But how does it work?

House hacking involves purchasing a multi-unit property, like a duplex, triplex, or quadplex, and living in one of those units while renting out the others. The income generated from these rented units can either significantly reduce or, in some cases, completely cover the property’s mortgage, taxes, and maintenance costs.

Here’s where the FHA loan comes into play: This loan type, backed by the Federal Housing Administration, is particularly favorable for house hackers because of its lower down payment requirements. So, instead of waiting years to save up a substantial down payment with an FHA loan, aspiring real estate investors can jumpstart their journey into property ownership and investment.

House hacking is more than just a smart move; it’s also a fantastic learning experience. As an owner-occupier of a multifamily property, you get firsthand experience in property management, tenant relations, and real estate maintenance—all without committing to full-time real estate investment. It’s a unique blend of personal residence and investment property, allowing you to get your feet wet in real estate without diving headfirst.

For many, FHA house hacking is the perfect introduction to real estate investment, offering a balanced mix of safety, learning, and financial growth.

Why House Hack?

The concept of house hacking, particularly with an FHA loan, has gained immense popularity in recent years and for several compelling reasons. Let’s explore why this innovative real estate approach is making waves:

Financial Efficiency

The primary allure of house hacking lies in its financial benefits. By renting out a portion of your property, you allow your tenants to contribute toward your mortgage and other property-related expenses. Over time, this can significantly diminish or, in some cases, completely offset your housing costs. For many, this means faster mortgage repayment and the potential to funnel savings into other investments.

Real Estate Education

House hacking offers a unique learning curve. By managing a property and interacting with tenants, you gain invaluable insights into real estate. This hands-on experience provides a solid foundation for those considering scaling their real estate portfolio in the future.

Equity Growth

As you pay down your mortgage (with the help of your tenants), you’re building equity in your property. This is a form of forced savings that, combined with potential property appreciation, can contribute to substantial wealth growth over time.

Flexibility with FHA Loans

The Federal Housing Administration offers loans designed to assist homeowners in purchasing properties, with house hackers reaping the benefits. With reduced down payment requirements and more flexible lending criteria, FHA loans make it more attainable for individuals to venture into a real estate investment earlier in their financial journey.

Diversified Investment Strategy

House hackers achieve a diversified approach to real estate by balancing personal residence with property investment. It’s a safety net: even if the real estate market faces challenges, you still reside in your investment, adding a layer of security to your venture.

FHA house hacking is not just a strategy—it’s a lifestyle choice. It’s about smart financial planning, continuous learning, and setting the stage for a prosperous future in real estate. If you’re looking for a way to make your money work harder while gaining a foothold in the property market, house hacking might be your answer.

Using an FHA Loan to House Hack

Embarking on a house hacking journey using an FHA loan is an exciting and practical venture for those eager to tap into the real estate market. The Federal Housing Administration’s support of this loan type has unlocked doors for countless individuals to realize their dreams of property ownership and investment. Let’s delve deeper into the pros and cons of using an FHA loan for house hacking:

Pros of FHA Loans

- Low Down Payment: One of the most attractive features of an FHA loan is the lower down payment requirement. While traditional or DSCR loans might require 20% or more, FHA loans require as little as 3.5% down. This makes entering the real estate market more accessible and lessens the initial financial burden.

- Flexible Credit Score Requirements: FHA loans are renowned for their flexibility regarding credit scores. This means even if you have a less-than-perfect credit history, you might still qualify for a loan, making homeownership attainable for a broader audience.

- Cash-Out Refinance Opportunities: The FHA offers comparable cash-out refinance options for homeowners, enabling them to adjust their loan terms or tap into home equity when needed. These refinancing options can be particularly beneficial if market conditions change favorably.

Cons of FHA Loans

- Mortgage Insurance Premiums (MIP): One of the more significant downsides to FHA loans is the requirement for mortgage insurance, both upfront and annual. While this insurance protects lenders, it can add to the monthly costs for homeowners.

- Loan Limits: The FHA sets caps on the amount you can borrow, which might restrict some from purchasing properties in pricier areas.

- Property Condition Standards: FHA loans come with specific property standards. Any home purchased with such a loan must meet these conditions, which might limit the available property options and may lead to additional repair or upgrade costs.

Navigating the world of FHA house hacking requires a balance of understanding the immense benefits and potential challenges that come with these loans. However, using an FHA loan for house hacking can be a financially rewarding experience with the right approach and thorough research.

Can You House Hack Multi-Unit Properties with an FHA Loan?

One of the burning questions aspiring real estate investors often grapple with is the feasibility of house-hacking multi-unit properties using an FHA loan. The short answer? Absolutely. However, as with all real estate ventures, the details matter. Let’s dive into the specifics of using FHA loans for multi-unit property investments:

Owner Occupancy Requirement

The FHA has a clear stipulation that borrowers must occupy one of the units in the multi-unit property as their primary residence for at least a year. You can’t just purchase a property and rent out all the units immediately; you must reside in one.

Loan Limits Depending on Unit Count

The amount you can borrow via an FHA loan varies based on the number of units in the property. For instance, a quadplex might have a higher loan limit than a duplex. It’s crucial to consult your area’s latest FHA loan limits to ensure your desired property fits within these boundaries.

Property Standards

As mentioned in the previous section, any property purchased with an FHA loan must meet specific health and safety standards. This can sometimes mean additional scrutiny for multi-unit properties, given the increased complexity of such properties.

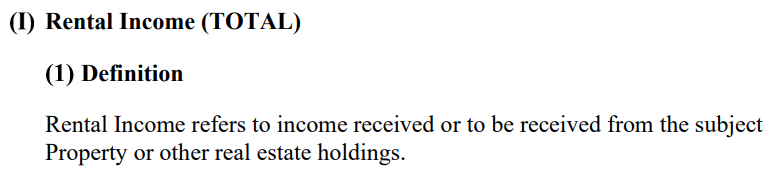

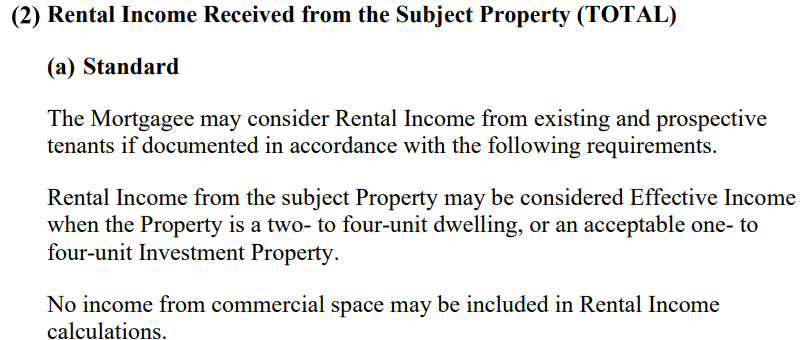

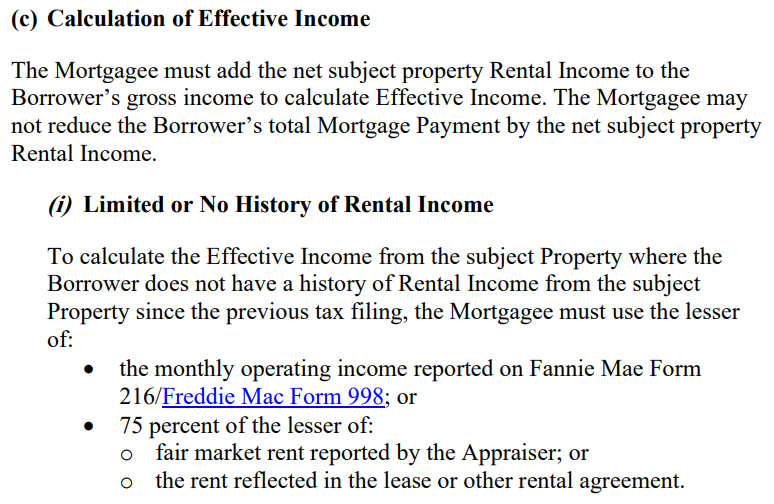

Rental Income Considerations

A silver lining for house hackers is that the FHA allows a portion of the anticipated rental income (typically 75% of market rent) from the other units to be considered in the borrower’s income calculations:

For calculation purposes, the underwriter will always place the borrower in the largest unit.

Adding rental income to your income for underwriting purposes can boost your borrowing power. However, it’s essential to note that there are guidelines and limitations are in place.

Insurance and Other Costs

Multi-unit properties might come with higher insurance premiums and additional maintenance expenses. While the rental income can help offset these costs, it’s essential to factor them into your calculations to gauge the property’s true profitability.

While the FHA makes it possible to house-hack multi-unit properties, potential investors must be well-informed and prepared. Remember, every real estate investment is a balance of opportunity and responsibility. With the proper knowledge, house-hacking multi-unit properties can be a stepping stone to long-term financial growth and stability.

Related: FHA Self-Sufficiency Test

FHA House Hacking and Short-Term Rentals

Diversifying rental strategies can amplify profits, leading house hackers to ponder the viability of offering their units as short-term rentals, akin to Airbnb or Vrbo models. However, when you use an FHA loan, there are guidelines and requirements to be keenly aware of.

HUD-92561

One of the critical forms associated with FHA loans is the HUD-92561. Essentially, this form is a borrower’s certification, stating that the multi-unit property financed with an FHA loan will not be used for transient or hotel purposes. In simpler terms, while long-term leases are permissible, turning your units into daily or weekly vacation rentals would violate the terms of the FHA loan as indicated on this form.

Local Laws and HOA Regulations

Beyond FHA stipulations, short-term rentals are also governed by local laws and regulations. Some municipalities have strict guidelines or even bans on short-term rentals. Similarly, if the property falls under a Homeowners Association (HOA), they might have their own regulations.

Insurance Implications

Using a unit for short-term rentals can change the insurance dynamics. Traditional homeowners or landlord policies might not cover liabilities or damages arising from short-term guests. It’s pivotal to consult with your insurance provider and consider specialized short-term rental insurance if you tread this path after refinancing your FHA loan into a DSCR or conventional loan.

Tax Considerations

The tax implications for short-term rentals can differ from long-term leases. Your tax obligations might change depending on the duration, guests’ stay, and the total days the property is rented out. Engaging a tax professional to understand these details is advisable.

While the allure of short-term rentals is undeniable, FHA house hackers must tread cautiously. Violating FHA terms or overlooking local regulations could lead to complications.

Next, let’s explore the benefits of house hacking.

What are the Benefits of House-Hacking?

While we’ve touched upon some of the advantages earlier, it’s worth diving deeper into the myriad of benefits that house hacking offers, especially when leveraging FHA loans. Let’s unpack the compelling reasons that are drawing a growing number of aspiring real estate investors to this strategy:

Reduced Living Expenses

Arguably the most significant draw, house hacking allows homeowners to cut down or even eliminate their housing costs. The rental income generated from other units can offset mortgage payments, property taxes, insurance, and maintenance expenses.

Accelerated Wealth Creation

By slashing living expenses, you can redirect funds towards other investments, savings, or paying down the property’s mortgage faster. Over time, this compounded saving, and investment can lead to accelerated financial growth.

Gaining Asset Management Experience

House hacking is an excellent sandbox for those new to real estate. Dealing with property maintenance, tenant relationships, lease agreements, and more provides invaluable experience without the pressure of managing a standalone investment property.

Portfolio Diversification

Real estate, especially a property where you reside, adds a tangible asset to your portfolio. As market trends fluctuate, having a diversified portfolio can offer stability and reduce financial risks.

Potential Property Appreciation

Over the long term, real estate typically appreciates. So, while you’re benefiting from rental income, the property itself could steadily increase in worth, leading to a handsome payday if you decide to sell.

Tax Advantages

Real estate offers several tax benefits, from deductions on mortgage interest to expenses related to property management. Furthermore, the structure of your rental income and expenses can provide tax efficiencies.

While house hacking, primarily through FHA loans, requires careful planning and a commitment to property management, the benefits are manifold. From financial advantages to personal growth and community building, FHA house hacking is more than just a real estate strategy; it’s a transformative lifestyle choice.

FHA House Hacking Example

Understanding FHA house hacking, in theory, is one thing, but seeing a tangible example can offer clarity and inspire potential investors. Let’s walk through a hypothetical scenario to see FHA house hacking in action:

Meet Liz:

Liz is a young professional looking to invest in real estate. After researching, she discovers the concept of FHA house hacking and decides to give it a go. Here’s her journey:

Property Purchase

Liz identifies a triplex in an emerging neighborhood priced at $300,000. Given the FHA’s low down payment requirement, she puts down 3.5%, amounting to $10,500.

Mortgage and Expenses

With her FHA loan, Liz’s monthly mortgage payment, including taxes, insurance, and Mortgage Insurance Premium (MIP), comes to $1,500. Other monthly expenses like maintenance, utilities for common areas, and miscellaneous costs total $300, bringing her monthly housing costs to $1,800.

Rental Income

Liz decides to live in one of the units and rents out the other two. Each rented unit brings in $1,000 monthly, totaling $2,000 in monthly rental income.

Net Monthly Costs

After accounting for rental income, Liz’s monthly housing cost is effectively reduced to a negative balance of $200. This means she lives for free and profits $200 each month.

Long-Term View

Over the years, as the neighborhood develops and demand grows, Liz can gradually increase the rent. Additionally, her property appreciates, and her equity in the triplex grows.

Exit Strategy

After several years, Liz decides to move to a single-family home. Instead of selling the triplex, she rents out the unit she lived in for $1,200 per month. Her monthly income from the triplex is $3,200, while her expenses, including mortgage, remain relatively stable, amplifying her monthly profit.

Key Takeaways

- The FHA loan’s low down payment requirement enabled Liz to invest in real estate with minimal upfront capital.

- Rental income not only covered her monthly expenses but also generated a profit.

- Long-term appreciation and increased rental demand further boosted Liz’s return on investment.

- House hacking provided Liz with a place to live and a growing asset.

Frequently Asked Questions

The Wrap Up

As we journeyed through the multifaceted world of FHA house hacking, it’s evident that this strategy offers a unique blend of benefits, especially for budding real estate investors. With its low entry barriers and inherent advantages, it’s no wonder that many, like Liz, are leveraging this avenue to secure a roof over their heads and lay the foundation for a prosperous financial future.

Key Takeaways

- Understanding FHA House Hacking: This is not just about buying a multi-unit property; it’s about strategically using the FHA loan system to reduce living costs while generating rental income.

- Benefits are Manifold: From slashing housing costs to gaining firsthand real estate experience and building community, FHA house hacking presents a multi-dimensional advantage.

- Regulations are Crucial: While turning units into short-term rentals may be tempting, adhering to FHA and local regulations, like HUD-92561, is paramount.

- Real-life Application: Liz’s story showcases the tangible potential of this strategy. Starting with a modest down payment, she achieved reduced living costs and positioned herself for long-term financial gains.

- Future Flexibility: After the primary residency obligation, investors have flexibility. The options are diverse, whether they transition the property into full-time rentals, sell for a profit, or refinance.

To any aspiring real estate investor, FHA house hacking is more than just a buzzword; it’s a stepping stone into the vast realm of property investment. It allows individuals to test the waters, gain experience, and understand the intricacies of real estate, all while reaping tangible rewards.

As with any investment strategy, due diligence, consistent research, and staying updated with regulations is key. But for those willing to commit, the horizon is ripe with opportunities.